17 INVESTMENT PROPERTIES (CONTINUED)

Description of valuation techniques used and key inputs to valuation on investment properties.

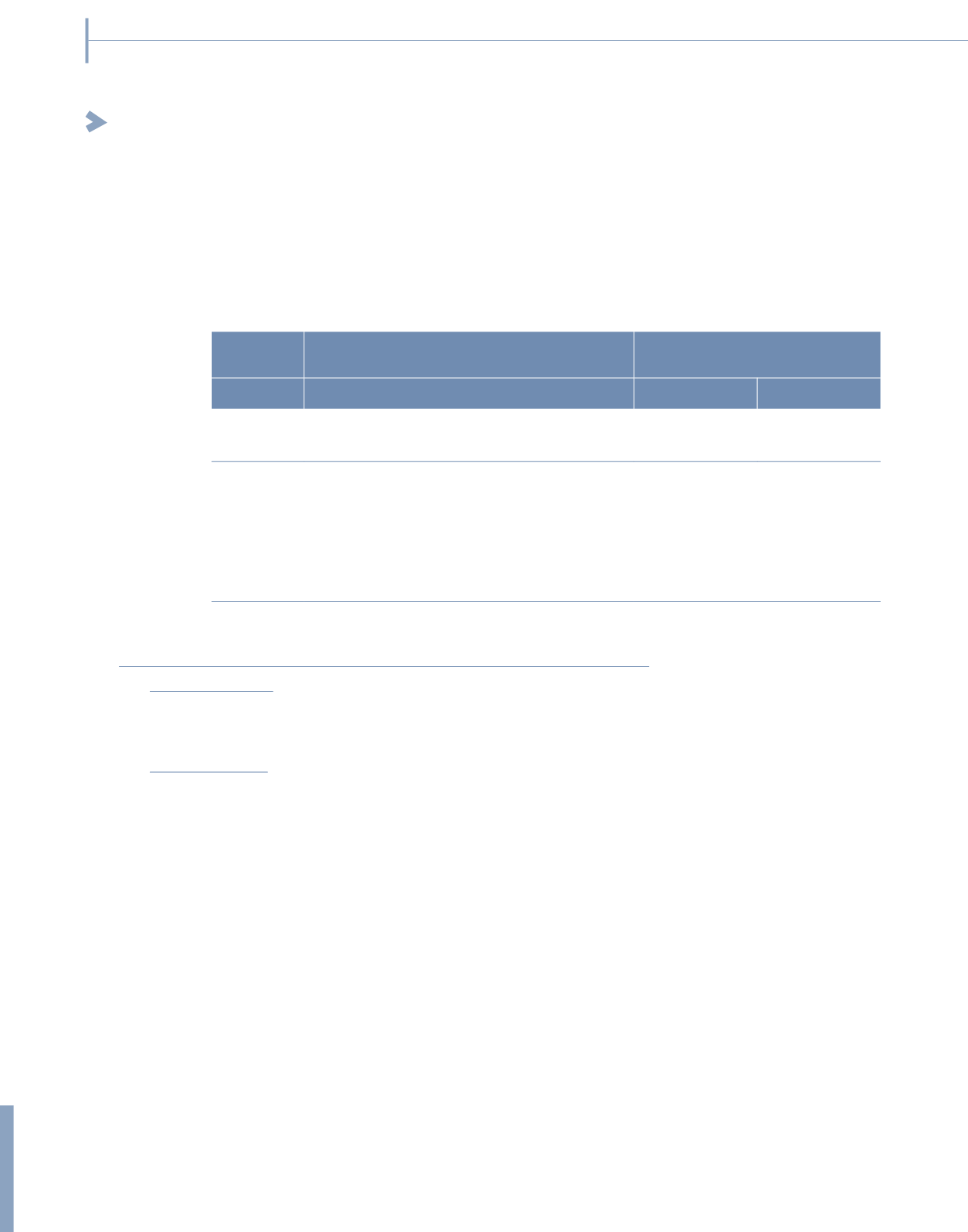

Valuation

technique Significant unobservable inputs

Range (weighted average)

2015

2014

Land and

buildings

Comparison

method Location, visibility, size and tenure

–

–

(Carrying value as at 31 December 2015 of RM69,179,000)

Office

properties

Investment

method

Estimated rental value per sqft per month

RM3.00 – RM4.00 RM3.00 – RM3.80

Outgoings per sqft per month

RM1.45 – RM1.52 RM1.45 – RM1.56

Void rate

5%-7.5%

5%-10%

Term yield

6%-6.25%

6.2%-6.5%

(Carrying value as at 31 December 2015 of RM210,654,000)

Inter-relationship between significant unobservable inputs and fair value measurement

(a) Comparison method

Generally a location and visibility that is relatively more prominent will result in a higher fair value. A longer tenure will

have the same effect.

(b) Investment method

Increases/(decreases) in estimated rental value per sqft in isolation would result in a higher/(lower) fair value of the

properties. Increases/(decreases) in the long-term vacancy rate (void rate) and discount rate (term yield) in isolation

would result in a lower/(higher) fair value.

Generally, a change in the assumption made for the estimated rental value is accompanied by a directionally similar

change in the rental value per sqft and an opposite change in the void rate and term yield.

A sensitivity analysis has been performed on the significant assumptions that impact the fair value of the office

properties. Arising thereof, the impact of a 10 basis points increase/decrease in the term yield will result in a lower/

higher fair value charge by RM3 million, while a void rate of 10% will result in a lower fair value charge by RM3 million.

282

NOTES TO THE

FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2015 (CONTINUED)